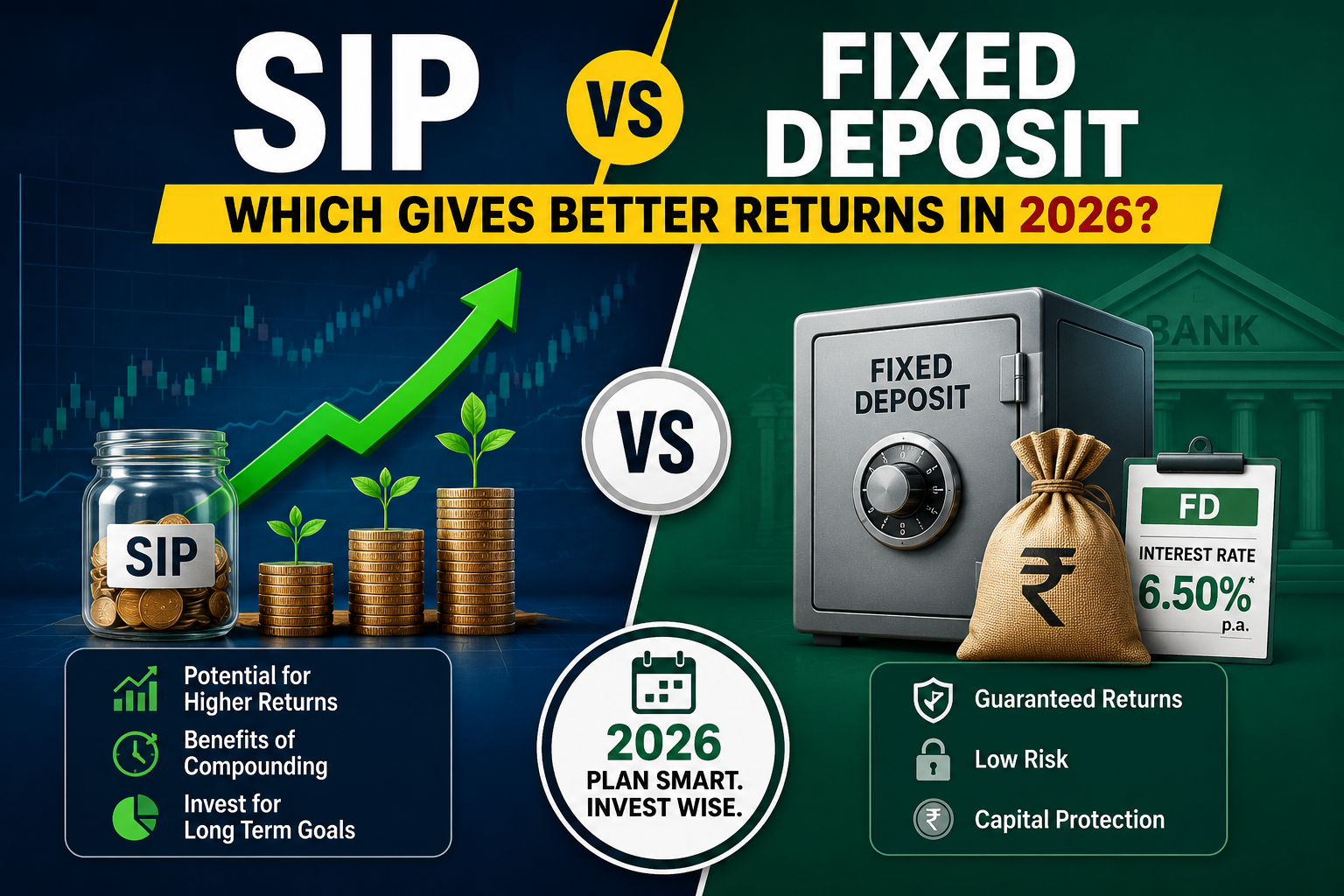

Every few months someone in a family WhatsApp group shares a screenshot. Either a mutual fund app showing 18% returns on a three-year SIP or a news headline about market crashes wiping out retail investor portfolios. The conversation that follows is usually the same. Should we just stick to FDs?

It is a fair question. Both SIPs and fixed deposits exist for good reasons, and the honest answer to “Which is better?” is not a single number it is a combination of what you need the money for, when you need it, and how much stress a falling portfolio gives you at 2 AM.

This article runs through both options with real numbers, actual trade-offs, and no promises about what the market will or will not do.

Understanding SIP and Fixed Deposit

What Is a SIP?

A systematic investment plan is not itself an investment product it is a method. You pick a mutual fund and instruct your bank to transfer a fixed amount, say ₹5,000, into that fund automatically every month. The fund uses that money to buy units at whatever the current market price is.

Some months you buy fewer units because markets are high. Some months you buy more because markets have fallen. Over time, this averaging effect called rupee cost averaging tends to smoothen the impact of market volatility.

The returns from a SIP depend entirely on the performance of the mutual fund chosen, which depends on the performance of the underlying securities, stocks, bonds, or a mix. There is no guaranteed return. There is no capital protection. What we have seen in the past is that investments can do better than inflation over time. This does not mean that the same thing will happen in the future. The people who manage these investments always say that what happened before does not guarantee what will happen next. They are not just saying this to follow the rules. Investments have the potential for returns that outpace inflation over periods.

What Is a Fixed Deposit?

A fixed deposit is what it sounds like. You give a bank a lump sum of money for a fixed period of time like six months or one year or five years. The bank pays you a certain amount of interest. This interest rate is decided when you open the fixed deposit. When the fixed deposit matures, you get your money along with the interest you earned from the fixed deposit.

The rate is locked when you book the FD. If rates fall during your tenure, your return does not change, which is an advantage. If rates rise significantly, you are stuck at the lower rate until maturity, which is a disadvantage.

No market exposure. No volatility. The number you see at the time of booking is the number you will get, minus taxes.

SIP vs Fixed Deposit – Quick Comparison

| Feature | SIP (Mutual Fund) | Fixed Deposit |

|---|---|---|

| Returns Potential | Market-linked; historically 10-14% p.a. in equity over long periods, but no guarantee | Fixed, typically 6.5-7.5% p.a. in 2026 depending on bank and tenure |

| Risk Level | Moderate to High (equity); Low to Moderate (debt funds) | Very Low |

| Capital Protection | No, NAV can fall below investment value | Yes, principal is protected |

| Liquidity | Generally liquid with exit load in early period; ELSS locked for 3 years | Premature withdrawal allowed with a penalty. |

| Taxation | LTCG tax after 1 year at 12.5% above ₹1.25 lakh gain; STCG at 20% for equity funds | Interest fully taxable as per income slab; TDS applicable |

| Investment Horizon | Best for 5 years and above | Flexible 7 days to 10 years |

| Inflation Protection | Better over long term if equity returns sustain | Partial real return, often 1-2% after inflation |

| Suitable For | Long-term goals, wealth creation, younger investors | Short-term goals, emergency fund, conservative investors, senior citizens |

Returns Comparison: What the Numbers Actually Show

People usually talk about the return on equity mutual funds being around 10 percent to 14 percent every year for ten years when they invest in big companies or a mix of different companies. This number is based on what happened in the past. It does not mean that the same thing will happen in the ten years. If someone says that it will definitely happen, they are not being honest about the equity funds. The return on equity funds is what we are talking about here, and we need to be careful when looking at the return on equity mutual funds.

Bank FDs in 2026 are offering anywhere from 6.5% to 7.5% depending on the bank and tenure. Small finance banks are going higher, some touching 8-8.5% on specific tenures. These returns are guaranteed as long as the bank remains solvent and deposits are within DICGC limits.

The gap between 7% guaranteed and 12% historical average sounds straightforward. It is not.

A 12% average return over a period means that there were some really bad years. For example, the Sensex went down by 30 to 40% in 2008, 2020, and early 2022. If someone got scared and sold their shares during those times, they did not get 12 percent. They might have only earned 2%. Even lost money.

The 12% average only happens for people who kept their money invested in the stock market during the years. Many people find it hard to do that. They thought it would be easier to stay calm and keep their shares when the market is doing well. When the market drops, it can be really tough to hold on to the shares. People who invest in the stock market need to be prepared for the years and keep their money invested in the stock market.

Example Investment Scenario

These are illustrative calculations only. Actual returns will vary, and mutual fund returns are not guaranteed.

Say Meena starts a ₹5,000 per month SIP in a diversified equity mutual fund, and her cousin Suresh puts ₹5,000 per month into an FD (or a recurring deposit). Both do this for ten years. Neither touches the money.

At 7%: what a recurring deposit or FD ladder might realistically earn Suresh’s ₹6 lakh of principal grows to approximately ₹8.6 lakh over ten years.

At 11%: a reasonable mid-point historical equity SIP estimate of Meena’s ₹6 lakh of principal grows to approximately ₹10.3 lakh.

At 6%: if Meena’s fund underperforms, both outcomes would be broadly similar. At 14% a good decade, her corpus touches ₹12.5 lakh.

The range for Meena is wide. The outcome for Suresh is narrow. That is the fundamental trade-off predictability versus potential.

Inflation: The Factor Most People Ignore Until It Is Too Late

The Consumer Price Index inflation in India has been increasing by 5 to 6% every year for most of the 2020s. This is what it means: the one lakh rupees that you have today will only be able to buy things that cost seventy-four thousand rupees in five years if the Indian Consumer Price Index inflation stays at 6%.

An FD earning 7% gives a real return of about 1-2% after inflation. That is positive your money is growing in real terms but not dramatically.

An equity SIP earning 11-12% over the long run gives a real return closer to 5-6% after inflation. That is the difference between doubling purchasing power over fifteen years versus barely maintaining it.

For someone parking emergency funds or saving for a goal twelve months away, inflation is not the main concern safety and accessibility are. For someone saving for retirement thirty years away, ignoring inflation is genuinely dangerous.

When SIP Makes More Sense

If you are in your twenties or thirties, saving for retirement SIP in a diversified equity fund is almost certainly the right vehicle. The time horizon is long enough to absorb multiple market cycles. The compounding effect over 25-30 years is real and significant.

For goals that are at least five years away, such as a child’s higher education, buying a house, or building long-term wealth equity, SIPs give the return potential that FDs simply cannot match over those timeframes.

If you have already built an emergency fund and your basic financial safety net is in place, incremental savings beyond that are better deployed in market-linked instruments for most working-age investors.

When Fixed Deposit Makes More Sense

Your emergency fund, three to six months of expenses, should be in an FD or high-yield savings account. Not in a mutual fund. Markets can be down exactly when you need the money most.

Goals that are twelve to thirty-six months away are FD territory. Planning to buy a car in eighteen months? FD. A family wedding two years from now? FD. You cannot afford to have the corpus down 20% the month before you need it.

Senior citizens and retirees drawing income from their savings belong in FDs. Predictable quarterly interest payments, capital safety, and no market anxiety are worth the lower nominal return at that life stage.

Anyone who loses sleep when investment apps show red numbers should have more of their money in FDs. Returns do not matter if anxiety causes you to redeem at the wrong time.

Common Mistakes Investors Make

Starting a SIP without a goal in mind and redeeming the moment it goes negative. This is the most common one. SIPs in equity funds are designed for long periods treating them like FDs and panic-redeeming at the first dip destroys value.

Putting emergency money in a mutual fund. The two-month wait for redemption plus the possibility that markets are down when you need the cash makes this a bad idea.

Ignoring taxation. FD interest is taxed as income at your slab rate. For someone in the 30% bracket, a 7% FD effectively earns 4.9%. An equity mutual fund held for more than a year pays a 12.5% LTCG tax on gains above ₹1.25 lakh, which for most small investors means effectively zero tax for several years. The taxation difference is real and often overlooked.

Assuming SIP means guaranteed returns. It does not. A fund can give 0% or even negative returns over three years. It has happened.

Example Reader Scenario

*This is an illustrative educational example, not a verified account.*

Rakesh Gupta, 38, works in Pune as a supply chain manager. He had ₹10 lakh in a savings account earning 3.5%, money he described as “just sitting there doing nothing.” He wanted to move it somewhere better but could not decide between an FD and a SIP.

He listed what the money was actually for. ₹4 lakh was his emergency fund money he might need any month. ₹3 lakh was for his daughter’s school admission fees in two years. ₹3 lakh had no specific purpose.

The emergency fund question answered itself. FD, immediate. He split it across two bank FDs to keep amounts within DICGC comfort levels.

The ₹3 lakh for school fees also answered itself. Two-year horizon, known requirement, cannot risk a market fall. FD, twelve-month renewable.

The last ₹3 lakh is where it got really interesting. There was no goal in mind, no specific timeline, and this money was something he could afford to not have for ten years. He decided to start a ₹5,000 Systematic Investment Plan in a large-cap index fund. Then he put the remaining amount as a lump sum into a mutual fund to be invested gradually.

What he said afterward was, “I was trying to pick one. I did not realize each chunk of money had a different answer.”

Taxation: The Part That Changes the Actual Numbers

FD interest is added to your total income and taxed at your applicable slab rate. If you are in the 30% bracket, your 7.5% FD returns 5.25% after tax. Banks take 10% tax on fixed deposit interest that’s more than ₹40,000 in a year. You can get this tax back. Adjust it when you file your taxes.

For equity funds, if you sell your units within one year, you have to pay 20% tax on the profit you make. Long-term gains beyond twelve months are taxed at 12.5%, but only on gains exceeding ₹1.25 lakh in a financial year. For small investors, this means several years of zero effective tax on equity fund gains.

Debt mutual funds no longer get indexation benefits they are now taxed at your income slab rate regardless of holding period. This makes them less tax-efficient than they used to be for most investors.

These tax numbers matter when comparing actual take-home returns. Always check current tax rules they have changed several times recently and can change again.

Expert Tips Before Choosing

Define the goal first. A goal without a timeline is not a goal it is a wish. Once you know when you need the money, the right product usually becomes obvious.

Build the emergency fund before anything else. Nothing market-linked until this is in place.

Do not put everything in one place. A mix of SIPs for long-term goals and FDs for near-term and emergency needs is what most financial planners actually recommend, not a binary choice.

Review annually not monthly. Checking your SIP NAV every week is how people make bad redemption decisions. Once a year is enough for most investors.

Start small and build. A ₹2,000 monthly SIP that you maintain through a market fall teaches you more about your own risk tolerance than any quiz can.

FAQs

Q1. Is SIP safer than FD?

No. SIPs in equity mutual funds carry market risk. FDs carry virtually no market risk. Safer is not the same as better it depends entirely on your goal and time horizon.

Q2. Can SIP guarantee returns?

No. Mutual fund investments do not offer guaranteed returns. Past performance is indicative only.

Q3. Which is better for retirement planning?

If you have fifteen or more years before you retire, equity SIPs have usually given you returns when you consider the effect of inflation on your money. If you are going to retire in five years or less, it is more important to keep your money safe, and fixed deposits become a better option for you. Equity SIPs are still a choice for people who have a long time before they retire because they have given better returns over time when you account for inflation.

Q4. Can I invest in both SIP and FD?

Yes, and for most people, this is the sensible answer. Different money for different purposes.

Q5. Which option beats inflation more effectively?

Equity SIPs have historically beaten inflation more significantly over long periods. FDs provide partial protection, positive real returns, but modest ones.

Q6. Are SIP returns taxable?

Yes. Equity fund gains held under twelve months are taxed at 20% (STCG). Gains held over twelve months are taxed at 12.5% on amounts exceeding ₹1.25 lakh annually (LTCG). Check current rules before investing.

Q7. Is FD suitable for emergency funds?

Yes, it is one of the best vehicles for emergency funds. Accessible, safe, and earning some return. Premature withdrawal comes with a small penalty, but it is worth having the option.

Q8. What if I want returns better than FD but do not want full equity risk?

Balanced or hybrid mutual funds invest in a mix of equity and debt.

Conclusion

There is no winner here. The question “SIP or FD?” only has a clean answer once you add three more pieces of information: what is the money for, when do you need it, and how much volatility can you handle without making bad decisions?

Emergency fund and near-term goals FD. For long-term wealth and goals that are five-plus years away, equity SIPs have historically made more sense. Senior citizens and conservative investors FD for its predictability.

For most working-age Indians, the answer is not either-or. It is both, each doing the job it is designed for. A ₹10 lakh corpus split thoughtfully between an FD for safety and an SIP for growth is likely more useful than putting all of it in whichever option gave better returns last year.

Figure out what the money is for. The rest follows.

Looking for the latest updates on personal finance, government schemes, banking news, investment guides, and economic developments? Visit BenefitsIndia.com regularly for trusted updates and easy-to-understand guides.